An obligation linéaire is just a fancy name for a linear bond. It is a simple debt tool used by big players like governments and companies. These bonds help them get cash for big projects while giving you a steady check. In the world of finance, these are known for being very clear and easy to trust. Both the person borrowing and the person lending know exactly what to expect.

Introduction to Obligation Linéaire

An obligation linéaire is a bond that follows a straight line. This means the interest and the money you get back are predictable. Governments have used these for a long time to build roads and schools. Companies also use them to grow their business without any hidden surprises. They are a major part of how the world handles debt today.

The basic idea is all about keeping things steady. Unlike some wild investments, these do not change their rules halfway through. This makes them very important for big money markets everywhere. Investors love them because they offer a safe place to park their cash. It is one of the most reliable ways to see your money grow over time.

What Is an Obligation Linéaire in Finance

In simple terms, an obligation linéaire is a promise to pay you back. The person who sells the bond agrees to pay you regular interest. This interest is often called a coupon. At the very end, they give you back the full amount you lent them. Everything follows a clear and simple schedule.

This bond is a contract between you and the borrower. You are basically acting like a bank for them. Because it is linear, the payments do not jump around. This is way different from complex bonds that have weird formulas. Most people find this much easier to understand and manage.

Linear bonds are the bedrock of safe investing. Big groups like pension funds put a lot of money into them. They do this because they need to know the money will be there later. It is a smart move for anyone who hates taking big risks. You get a clear path to your financial goals.

Core Characteristics of Obligation Linéaire

There are a few things that make an obligation linéaire stand out. First, the interest rate is usually fixed or very clear. You know exactly how much you will make every year. Second, the payments happen on a set calendar. This helps you plan your own budget perfectly.

- Fixed Interest Rates help you lock in your earnings for years.

- Scheduled Payments mean you never have to guess when cash arrives.

- Maturity Dates tell you the exact day you get your principal back.

- Standardized Rules make it easy to sell the bond to someone else.

- Legal Protections give you peace of mind that the contract is solid.

These traits make the bond very easy to trade. Because everyone knows the rules, finding a buyer is simple. This is called market liquidity, and it is a big plus. It also makes it easy to see if you are getting a good deal. Simple bonds are often the most honest ones.

How Obligation Linéaire Works

Everything starts during the issuance phase. This is when the borrower asks for money from the public. They set the interest rate and the end date. Investors buy the bonds and the borrower gets the cash they need. It is a win-win for both sides.

Once the bond is live, it enters its lifecycle. Every year or six months, you get your interest payment. This continues until the bond reaches its maturity date. On that final day, you get your original investment back. The process is smooth and very predictable.

Predictability is the secret sauce here. You can use these bonds to plan for big life events. Maybe you want to pay for college or retire comfortably. Big companies use them to match their own future bills. It is all about making sure the money shows up on time.

Diverse Types of Obligation Linéaire

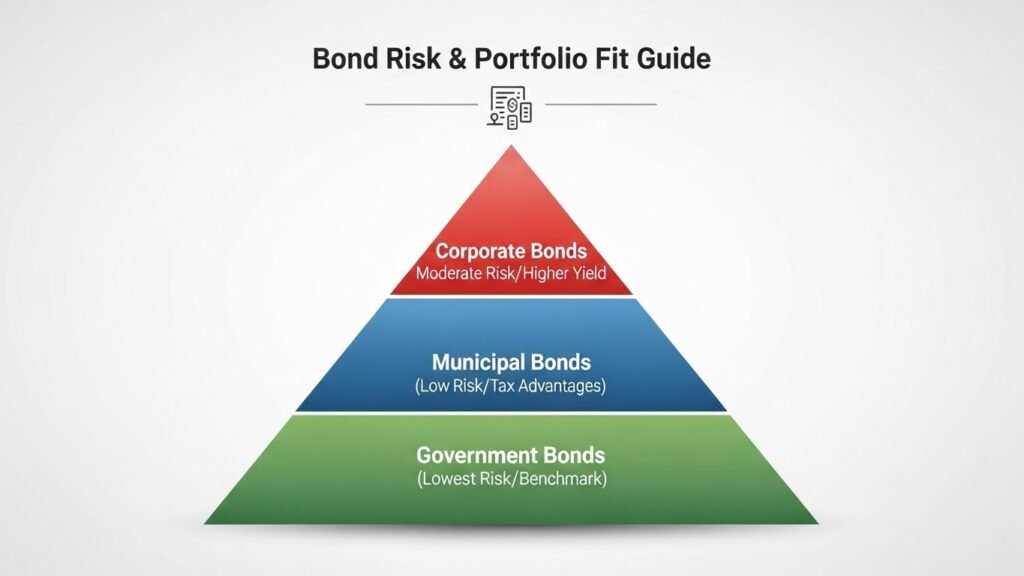

Government Linear Bonds

Governments use these to pay for things like hospitals and parks. They are usually seen as the safest type of bond. Since a country can tax its people, it is likely to pay you back. Many people use these as a benchmark for all other investments. They are the gold standard of the bond world.

Corporate Linear Bonds

Companies sell these bonds to build new factories or buy other firms. They often pay a higher interest rate than governments. This is because a company is a bit riskier than a country. It is a great way for businesses to get long-term cash. Investors get a bit more profit for taking that extra risk.

Municipal and Agency Linear Bonds

Local cities or small agencies also issue linear bonds. They use the money for things like local water systems. These can sometimes have special tax breaks for you. They are a bit more niche but still very important. They help keep your local community running smoothly.

Indexed and Inflation-Linked Linear Bonds

Sometimes, prices for things like food and gas go up fast. These bonds help protect you from that inflation. The payments might go up if the cost of living rises. This keeps your money from losing its real value. It is like having a shield against rising prices.

Advanced Technical Metrics and Bond Math

Duration and Modified Duration

Duration is a way to measure how much a bond’s price moves. If interest rates in the market change, your bond price might too. A higher duration means the price is more sensitive. It helps you understand the risk of interest rate swings. Knowing this number makes you a much smarter investor.

Convexity in Linear Bonds

Convexity is a bit more advanced but still useful. It shows how the duration changes as rates move. Most linear bonds have a nice shape to their price moves. This “curve” can actually help protect your investment. It is a technical way to see how the bond reacts to the world.

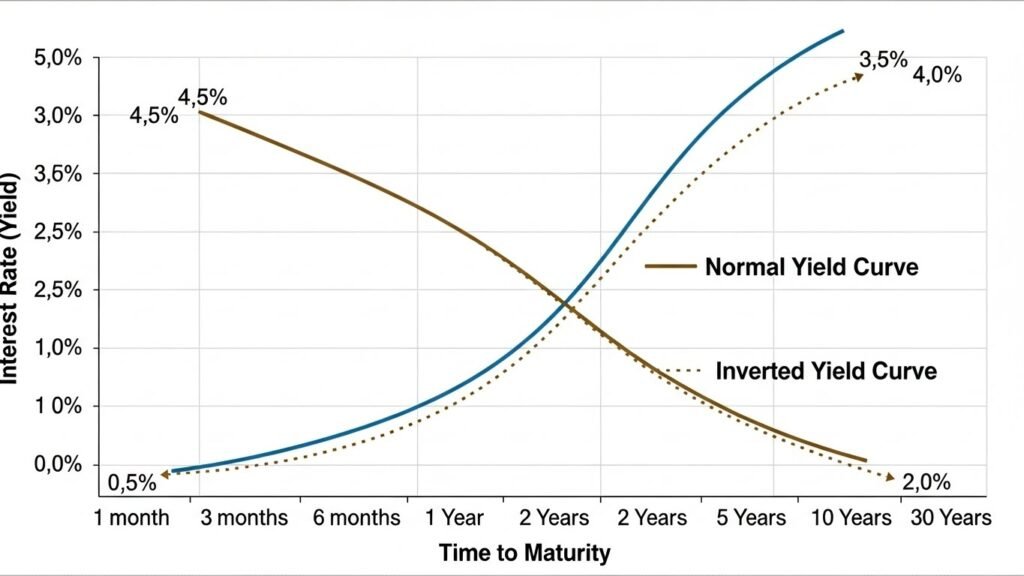

The Yield Curve and Linear Bonds

The yield curve is a map of interest rates over time. It shows what you can earn on short-term vs long-term bonds. When the curve changes, it tells a story about the economy. Linear bondholders watch this very closely. It helps them decide if it is a good time to buy or sell.

Valuation and Pricing of Obligation Linéaire

Pricing a bond is all about looking at future cash. You take all the future payments and see what they are worth today. This is called discounted cash flow analysis. If market rates go up, your old bond might look less attractive. That is why the price goes down when rates rise.

- Yield to Maturity is the total return you expect if you hold to the end.

- Current Yield is just the annual interest divided by the bond price.

- Credit Spreads show the extra pay you get for taking on extra risk.

- Accrued Interest is the money the bond earned since the last payment.

When you buy a bond, you might pay more or less than its face value. This depends on how its interest rate compares to the market. It is a bit like shopping for a used car. You want to make sure the price is fair for what you get. Checking the credit rating of the issuer is a must.

Advantages of Obligation Linéaire for Investors

One of the best things is the peace of mind. You do not have to watch the stock market every day. The payments are stable and very easy to track. This makes it perfect for people who need a steady check. It takes the stress out of building your wealth.

- Stable Income makes it easy to pay your bills every month.

- Lower Risk compared to stocks means you sleep better at night.

- Diversification helps protect your whole portfolio from crashing.

- Collateral means you can sometimes use these bonds to get a loan.

Linear bonds are also very clear about the rules. There are no hidden fees or weird clauses to worry about. This transparency is rare in the financial world. It is a simple tool that does its job very well. Most people find them to be a very honest investment.

Risks and Mitigation Strategies

No investment is 100% safe, even a linear bond. The biggest threat is usually the interest rate risk. If rates jump, the market value of your bond might fall. You only lose money if you sell before the end. If you hold it until maturity, you still get your full principal.

- Credit Risk happens if the borrower goes broke.

- Inflation Risk can make your fixed payments feel smaller.

- Liquidity Risk means it might be hard to sell quickly.

- Reinvestment Risk is when you have to settle for lower rates later.

To stay safe, you should spread your money around. Do not put everything into just one bond. Buy bonds from different issuers and with different end dates. This is called a laddering strategy. It helps you stay flexible no matter what happens to rates.

Tax Implications and Regulatory Framework

Taxes can take a bite out of your bond earnings. Usually, the interest you get is taxed as regular income. If you sell the bond for a profit, you might owe capital gains tax. Every country has its own rules for this. It is smart to talk to a tax pro to keep more of your cash.

Big banks and insurance companies follow strict rules. They are often required by law to hold safe bonds. This helps make sure they have enough money to pay their own bills. These rules keep the whole financial system from breaking. Because linear bonds are so safe, they are perfect for this.

Many people hold their bonds in special accounts. These accounts might offer lower taxes or other perks. It is a great way to grow your money faster. Always check if your retirement account can hold these bonds. It could be a big boost for your future.

Obligation Linéaire vs Alternative Debt Structures

Linear bonds are much simpler than structured bonds. Structured bonds might pay more, but they are very confusing. Zero-coupon bonds do not pay any interest until the very end. This can make them much more volatile in price. Most people prefer the regular check from a linear bond.

- Amortizing Bonds pay back part of the principal with every check.

- Perpetual Bonds never have an end date and pay forever.

- Convertible Bonds can be turned into company stock later.

When you compare them, the obligation linéaire is the most direct. You know exactly when you get paid and when it ends. There are no “if” or “maybe” statements in the contract. This makes it much easier to plan your life. For many, simplicity is the greatest advantage of all.

Comparison of Different Types of Obligation Linéaire

This table breaks down the main types of linear bonds based on who issues them, their risk levels, and their primary goals.

| Bond Type | Primary Issuer | Risk Level | Main Purpose | Unique Feature |

| Government | National Governments | Very Low | Funding public infrastructure and debt | Considered the “risk-free” benchmark |

| Corporate | Private Companies | Low to Moderate | Business expansion and acquisitions | Higher yields to compensate for risk |

| Municipal | Cities or Local Agencies | Low | Local projects like schools or water | Often carries local tax advantages |

| Indexed | Governments or Corps | Low | Protection against rising living costs | Principal adjusted based on inflation |

Key Takeaways for Your Portfolio

- Government bonds are your best bet for maximum safety and capital preservation.

- Corporate bonds are great when you want to squeeze out a bit more profit and can handle a little extra risk.

- Municipal bonds help you support your own backyard while often keeping more cash away from the taxman.

- Indexed bonds act like a financial shield, making sure your money doesn’t lose its “buying power” over time.

How to Choose the Right One

Choosing the right obligation linéaire depends on your own goals and how much risk you can stomach. If you are close to retirement, you might lean heavily toward government or municipal bonds for that steady, safe check. If you are younger and building wealth, corporate bonds might give you that extra boost you need.

Most smart investors do not just pick one; they mix them together to create a balanced shield for their money. By holding a variety of these types, you protect yourself if one specific sector of the economy hits a rough patch. It is all about making sure your money is working as hard as you do.

The Evolution: Green and Social Linear Bonds

Lately, more bonds are being used for good causes. Green bonds help pay for solar panels and clean water. They follow the same linear structure as other bonds. The only difference is where the money goes. It is a great way to invest and help the planet at the same time.

Social bonds help build things like affordable housing. They are part of a trend called ESG investing. Many investors now want to know their money is doing good. These bonds offer the same safety with an added moral bonus. It is becoming a huge part of the global bond market.

Sometimes these green bonds have a slightly lower yield. This is because so many people want to buy them. This is called a “greenium” in the finance world. Even so, they remain a top choice for modern investors. You get to make money and make a difference.

Strategic Portfolio Construction

Building a bond portfolio is like building a house. You need a solid plan to make sure it lasts. Many people use a laddering strategy. This means you buy bonds that end in different years. Every year, one bond ends and gives you cash to reinvest.

- The Barbell Strategy uses both very short and very long bonds.

- The Bullet Strategy focuses all your bonds on one specific year.

A good plan helps you handle whatever the market throws at you. If interest rates go up, your short-term bonds will end soon. You can then take that cash and buy new bonds at the higher rate. This keeps your income growing over time. It is a very smart way to manage your wealth..

Risk Evaluation Checklist for Linear Bond Issuers

Before purchasing an obligation linéaire, use this checklist to assess whether the borrower fits your risk tolerance.

Creditworthiness and Financial Health

- Check the Credit Rating: Look for ratings from major agencies (like Moody’s or S&P) to see if the issuer is considered high-quality or speculative.

- Analyze the Debt-to-Income Ratio: For companies, check if they have enough profit to cover their interest payments without struggle.

- Evaluate Government Stability: For sovereign bonds, consider the country’s ability to tax its citizens or grow its economy to repay debt.

Bond Terms and Transparency

- Verify the Interest Structure: Confirm if the rate is fixed or indexed to ensure it aligns with your need for predictability.

- Review the Maturity Date: Ensure the date the principal is returned matches your long-term financial timeline.

- Identify Hidden Clauses: Check for “call” features that might allow the issuer to pay you back earlier than you planned.

Market and Environmental Factors

- Assess Interest Rate Sensitivity: Calculate the duration to see how much the bond’s price might drop if market rates rise.

- Consider Inflation Protection: Determine if you need an indexed bond to shield your “buying power” from rising costs.

- Review ESG Alignment: If the bond is a “Green Bond,” verify that the funds are strictly used for sustainable projects.

Portfolio Fit and Diversification

- Check Sector Exposure: Ensure you are not putting too much money into one specific industry, such as tech or energy.

- Review Your Bond Ladder: Confirm that the maturity of this new bond fits into your schedule of regular cash returns.

- Evaluate Liquidity Needs: Ask yourself if you can afford to keep the money locked up until the maturity date.

Comparison of Primary Risks

| Risk Type | What it Means | How to Mitigate |

| Interest Rate Risk | Market rates go up, bond price goes down. | Use a laddering strategy to stay flexible. |

| Credit Risk | The borrower cannot pay you back. | Stick to high-rated government or blue-chip bonds. |

| Inflation Risk | Your fixed check buys fewer goods over time. | Invest in indexed or inflation-linked bonds. |

| Liquidity Risk | It is hard to sell the bond quickly for a fair price. | Focus on standardized bonds with high market volume. |

Conclusion: The Enduring Importance of Obligation Linéaire

The obligation linéaire is a true classic in the finance world. Its simple and clear structure has stood the test of time. While other fancy investments come and go, this bond remains. It provides a bridge between people with cash and those who need it. This helps economies grow and helps people build a future.

For any investor, having a few linear bonds is a smart move. They act as a safety net for your more aggressive bets. You get the peace of mind that comes with a guaranteed contract. In a world that is often confusing, these bonds are a breath of fresh air. They are simple, honest, and very effective.

As you grow your wealth, remember the power of the straight line. You do not always need the most complex tool to win. Often, the most predictable path is the one that gets you there. The obligation linéaire is that path for millions of investors. It is a proven way to secure your financial legacy forever.

Disclaimer: This content is for educational purposes only. Please consult with a qualified financial expert or investment advisor before taking any action or making any investment decisions.

Frequently Asked Questions

What happens if I need my money before the maturity date?

If you need cash before the bond ends, you can sell it to another investor on the secondary market. However, the price you get depends on the current market interest rates at that time. If rates have gone up since you bought the bond, you might have to sell it for less than you paid.

Can a linear bond have a variable interest rate?

Generally, a linear bond is known for having a fixed and predictable rate. While some bonds are “indexed” to things like inflation, they still follow a linear repayment schedule where the rules are set from the start. This keeps the bond from having the “weird formulas” found in complex structured products.

What is the difference between the face value and the market price?

The face value is the amount the borrower promises to pay you back at the end. The market price is what people are willing to pay for that bond today. You might pay more than face value if the bond’s interest rate is higher than what the market currently offers.

Are these bonds protected by insurance like bank deposits?

No, linear bonds are usually not covered by government deposit insurance. Your safety depends on the creditworthiness of the borrower. This is why many investors view government bonds as the “gold standard” because a country can tax its citizens to pay back the debt.

How do credit ratings affect my linear bond?

Credit ratings act like a report card for the borrower. If a company or government gets a lower rating, it means experts think there is a higher risk they won’t pay. This usually causes the bond’s price to drop because new buyers will want a higher return for taking on that extra risk.

What exactly is a “coupon” in the context of these bonds?

A coupon is simply the regular interest payment you receive as a bondholder. In the past, physical bonds had paper coupons that you would clip and trade for cash. Today, these are handled digitally and sent straight to your account on a set schedule.

How does “accrued interest” work when buying a used bond?

If you buy a bond between two payment dates, the seller has already “earned” some interest for the days they held it. You typically pay the seller that earned portion up front. Then, when the next full payment arrives, you keep the whole check, which balances everything out.

Why do pension funds invest so heavily in obligation linéaire?

Pension funds have to pay out steady checks to retired people for many years. They use linear bonds because the payments are predictable and help them match the money coming in with the money they need to pay out. This keeps the fund stable and reliable.

Is a linear bond the same as a savings account?

Not exactly, though both pay interest. With a savings account, your principal usually stays the same, and you can withdraw it anytime. With a linear bond, you are locked in until a specific date unless you sell it to someone else. Also, the value of the bond can go up or down while you hold it.

Can the issuer pay back the bond early?

Some bonds have a “call” feature that lets the borrower pay you back sooner than expected, but this is less common in a standard obligation linéaire. True linear bonds usually stick to a strict and transparent schedule until the final maturity date.

What is “reinvestment risk” for a bondholder?

This risk happens if interest rates drop by the time your bond ends. When you get your big principal check back, you might find that new bonds pay much less than your old one did. This makes it harder to keep your total income at the same level.

How do I calculate the “Current Yield” of my bond?

The current yield is a quick way to see your annual return. You take the total interest you get in a year and divide it by the price you paid for the bond. It is a simple tool to see if the bond is a good deal compared to other options.

What makes a bond “liquid”?

A bond is liquid if it has standardized rules that everyone understands, making it easy to find a buyer quickly. Because linear bonds are so simple and common, there is usually a large market of people ready to buy and sell them.

Why would I buy a bond with a “greenium”?

A greenium means you accept a slightly lower interest rate to support a good cause, like clean energy. Many investors find the “moral bonus” worth the small drop in profit. It allows you to grow your wealth while also helping the planet.

What is a “Zero-Coupon” bond compared to a linear one?

A zero-coupon bond does not pay regular checks; instead, you buy it at a big discount and get one large payment at the very end. These are much more volatile because you have to wait a long time to see any cash. Most people prefer linear bonds for the regular, steady income.

Can I hold linear bonds in a retirement account?

Yes, and it is often a very smart move. Many retirement accounts offer tax perks that allow your bond interest to grow faster without being taxed right away. You should check with your account provider to see if they allow bond trading.

What is the “Barbell Strategy”?

This is a plan where you buy some bonds that end very soon and some that end a long time from now. The short bonds give you quick cash if you need it, while the long bonds usually pay higher interest rates. It looks like a barbell because the middle years are left empty.

Does inflation always hurt bondholders?

Inflation can be tricky because it makes your fixed interest checks feel smaller. However, if you have “inflation-linked” bonds, your payments actually go up when prices rise. This acts as a shield to keep your money from losing its real value.

What happens if the borrower goes through a merger?

If a company is bought by another firm, the new owner usually takes over the debt. Your contract remains valid, and the new company is now the one responsible for paying your interest and principal.

How do linear bonds help the overall economy?

They act as a bridge between people who have extra cash and groups that need it for big things. By providing a safe way for people to lend money, they ensure that schools, hospitals, and new businesses can get the funding they need to grow.